An emergency fund helps you handle sudden costs without falling into debt. Most money experts view this fund as the first step before any other money goals. Without this protection, even smart savers can find themselves in trouble quickly.

You might face many problems in life. This can be a job’s end without warning, leaving families scrambling to pay bills. Some health problems also have costs that insurance won’t fully cover. Small issues like vet bills or travel for family matters can strain tight budgets.

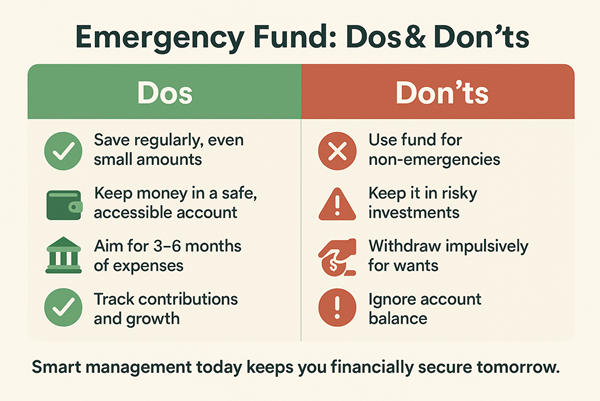

This money cushion gives you time to think clearly during stress. You can make smart choices rather than panic moves. You can save for three to six months of basic costs so that you can relax during rough patches.

Why Do You Need an Emergency Fund?

Job losses happen without warning, leaving families without income for weeks or months. Health problems bring bills that insurance won’t fully cover. You can have some money set aside so that it can help you survive in an emergency. This financial buffer turns major crises into manageable situations.

An emergency fund stops the debt cycle before it starts. People often turn to credit cards or loans during tough times without savings. These options seem helpful, but they create long-term money problems with high interest rates.

- Protects your home from foreclosure risks

- Keeps essential services running during hard times

- Gives you time to make better choices

- Shield your credit score from damage

- Creates a foundation for broader money goals

Most experts suggest saving three to six months of basic costs. You can start small with £500, then build toward one month’s expenses. You can start today, even with just £25 per week.

|

Emergency Fund vs. Regular Savings | ||

|

Feature |

Emergency Fund |

Regular Savings |

|

Purpose |

For urgent, unexpected needs |

For planned goals/purchases |

|

Access |

Quick and easy |

Flexible |

|

Risk Level |

Low risk, high liquidity |

Varies with account type |

|

Spending Rule |

Only for emergencies |

Can be used anytime |

5 Steps to Build an Emergency Fund

There are some steps you need to follow to build an emergency fund. This way you will be able to answer your financial questions like how to set financial goals, how to save money and more. Here are the steps:

Step 1: Set a Clear Goal

You can start by looking at your monthly costs. Most money experts suggest saving three to six months of basic living costs. This gives you time to recover if something bad happens.

A single person might need £5,000, while a family could need £15,000 or more. You can break this big number into smaller weekly or monthly goals.

Step 2: Review Your Budget

You can take time to track where each pound goes for a full month. Many free apps can help make this task easier. You look for costs you can cut without feeling too much pain.

Maybe you’re paying for services you rarely use. Or perhaps eating out less could free up cash. Starting a budget helps you understand the expenses of each month. This step often shows people they have more saving power than they thought.

Step 3: Open a Safe Account

You can pick a basic savings account or a money market account with easy access. You can look for accounts with no fees and quick access to your money. Some lenders offer special emergency fund accounts with slightly better rates.

The goal isn’t getting rich from interest but having money ready during any financial struggles. You can keep this account at a different bank than your checking account if possible. This small barrier helps stop you from dipping in for non-emergencies.

|

Where NOT to Keep Your Emergency Fund? | ||

|

Place |

Why Not? |

Better Alternative |

|

Stocks/Equity funds |

High risk of loss |

Savings account |

|

Retirement accounts |

Penalties for early withdrawal |

Money market account |

|

Real estate |

illiquid, can’t sell fast |

Fixed deposits (short term) |

|

Cash under mattress |

Theft, no growth |

Bank savings account |

Step 4: Save Regularly

You can set up auto transfers on payday before you spend the money. Even £20 a week adds up to over £1,000 in a year. You can treat this transfer like any other bill that must be paid.

You increase your savings amount before increasing your spending when you get a raise at work. This works better than waiting for “extra money” that rarely appears.

Step 5: Grow Your Fund Faster

You speed up your progress with smart moves that boost your savings. You can put any extra money straight into your fund before spending it. Work bonus? Tax refund? Birthday gift? All perfect for your emergency fund.

You look around your home for items you no longer need but others might value. You can sell all these online and turn clutter into safe money. You can consider ways to earn extra for a short time. This might mean weekend work, online tasks, or using a skill you enjoy. Then you can think about “how much you plan to spend?” during emergencies.

Can You Use Investments for an Emergency Fund?

The idea of growing your emergency money through stocks sounds smart at first. Why let cash sit earning tiny interest when markets might offer bigger returns? This thinking misses the core purpose of emergency savings.

Markets move up and down in ways nobody can predict. Your investments might drop 20% right when you lose your job or face a major home repair. This terrible timing turns a bad situation into a true crisis. Emergency funds must be rock-solid and reliable when you need them most.

Savings accounts offer something far more valuable than high returns, that is, certainty. The £1,000 you put in today will still be £1,000 when your car breaks down next month.

Many investments take days to sell and transfer to your bank account. This delay could mean missed rent payments or late medical care.

- Cash serves as your financial shock absorber

- True emergencies rarely give advance warning

- Market drops often happen alongside economic troubles

- Recovery time matters after using your funds

- Your emergency savings is insurance, not an investment

Once your emergency fund reaches your target amount, then investing might work. You can start building wealth through the markets with money beyond your safety net. This gives you both protection and growth potential.

What to Do After You Build It?

Your emergency fund can now protect you from life’s costly surprises. You keep these funds away from your everyday banking accounts. The mental wall between regular money and emergency cash helps stop casual dipping. Some people even choose banks across town to make access slightly harder.

You can review the size yearly or after big life events. New baby? You’ll need more backup cash. Paid off the car? Perhaps less. This yearly check takes just minutes but keeps your safety net right-sized.

You can look toward more exciting money goals with your emergency fund secure. Many people shift focus to retirement savings goals or mid-term plans like home buying. You can now take smart risks knowing you have backup. It protects while you build wealth in other ways. The small and steady steps can now build your future dreams just as effectively.

Conclusion

You can build your emergency fund by taking time. You can start small if needed; even £500 helps with many common problems. The goal isn’t speed but steady progress toward better protection. This money foundation lets you sleep better knowing you’re ready for what comes. Once built, this fund frees you to pursue bigger dreams without fear holding you back.

Having worked as a research analyst for 10 years, Archie developed his interest in consulting people struggling to manage money and now working as a Financial Consultant at Onestoploansolution. He is postgraduate in banking and accounting. For his a normal day starts from assessing the application and helping borrowers with getting more control over their finances. Archie Leo contributes to the finance blog of the company where he has written a lot of articles covering a wide range of topics such as budgeting, investing, saving and building wealth. His goal is to make people’s life easier with money.