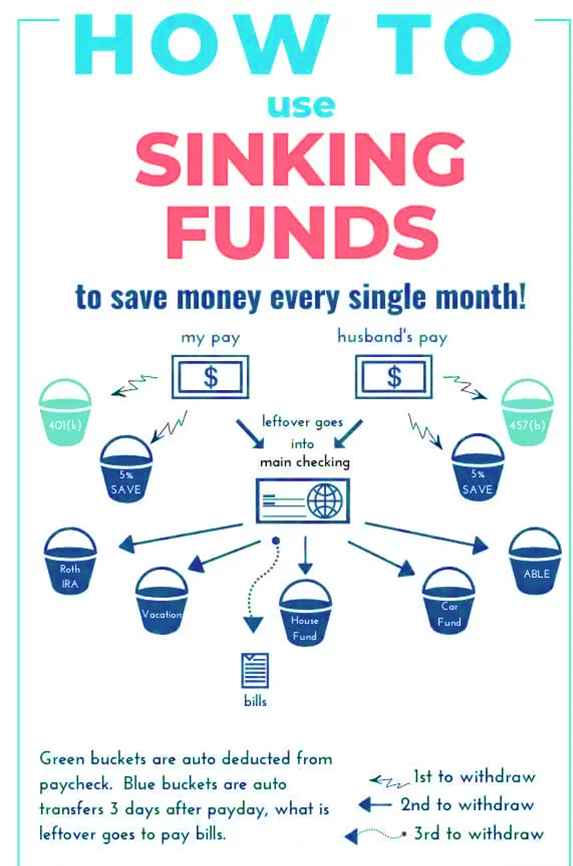

A sinking fund is a savings and investment technique aimed at accumulating money towards a particular life goal. It requires you to know the purpose, set a saving limit, and the timeline. You may also need to decide how much you need to put towards the sinking fund monthly.

Tapping into a sinking fund is a better option to cover your long-term and short-term goals without affecting your emergency fund. If you are confused regarding how to use sinking funds to save towards your goals, read ahead. The blog lists the step-wise process that may help you.

What do you mean by a sinking fund?

A sinking fund is a savings strategy to save money towards a specific and predictable expense. It could be saving for a wedding, furniture, car finance deposit, etc. One can begin by determining the purpose, the amount to save, and the time limit. Also, check the amount one can afford to save every month or week, depending on the liabilities.

It decides when you can achieve the target. For example, if you wish to buy a car and save £4000 monthly, you can save £24000 in 6 months. Thus, you must keep £4000 spare each month to save towards the goal. Thus, a sinking fund is a great way to save money without depending increasingly on credit cards.

Sinking Fund Vs. Emergency Funds: What’s the difference?

The basic difference between https://www.onestoploansolution.co.uk/blog/sinking-fund-vs-emergency-fund-whats-the-difference/https://www.onestoploansolution.co.uk/blog/sinking-fund-vs-emergency-fund-whats-the-difference/sinking funds and emergency funds is the PURPOSE. One uses a sinking fund for any known short-term or long-term specific goal. However, an emergency fund is only used to counter cashless situations or unplanned expenses. Here is the detailed difference between the two:

|

Sinking Funds |

Emergency Funds |

|

The amount you save may vary according to the purpose you want to save for |

One usually saves up a fixed amount for 6-8 months in an emergency fund. |

|

Examples of sinking funds include: ÿ Car insurance and tax ÿ Back-to-school costs ÿ Sabbatical costs ÿ House renovation ÿ A planned holiday |

Examples of emergency funds include: ÿ Sustain expenses post-unemployment ÿ Sustain the business loss ÿ Make important bill payments like rent and utility bills ÿ Countering unforeseen medical expenses |

|

It reduces the dependency on emergency funds, credit cards, and savings. |

It proves to be the best alternative to low-income cash emergencies. |

5 Steps to Use a Sinking Fund to Cover Your Specific Goal

Getting started with a sinking fund is easy once you are clear about the purpose. You can choose the type of savings fund to save towards the specific goal. The most common way to do that is by using a savings account. It is the simplest way to start saving for your goals. Here are the steps to follow:

Step 1 – Identify your goal

Prioritising your short-term and long-term goals is important before saving into a sinking fund. Identify the most important and immediate aim that you must achieve. It could be saving money to paint your living room.

Step 2- Decide how much to save

Once you know the purpose, determine how much you would need to achieve that. The amount may greatly vary accordingly. You may need to save £1000 for small repairs or £10000 for renovating car seat covers. Thus, arrive at a number accordingly.

Step 3- Analyse your budget

Identify how much you can realistically save given the required amount. Exercise restriction on spending carelessly, taking on new credit cards, etc. Instead, stick to the goal and try to save the desired amount. It helps you achieve the goal and boosts your credit score in the process. For example, if you need to save £10000 for car seat repairs and your monthly expenses are £15000. Here is how to cut:

|

Expenses to cut |

The amount you spend monthly (in pounds) |

How much should you ideally spend? (in pounds) |

|

Movies |

2000 |

500 |

|

Eating out |

3000 |

1500 |

|

Weekend gateways |

7000 |

4000 |

|

Total expenses per month |

12000 |

6000 |

Step 4- Decide the time frame

After analysing and adjusting the budget, decide on the timeline. By when can you achieve the goal comfortably? It may vary according to the income flexibility, monthly expenses, unexpected expenses, and amount required.

Calculate how much you can save each month as a fixed amount. For example, if you need £42000 within 6 months, you must save £7000 each month to achieve the goal.

Here, uncertain cash hiccups may affect the timeline. Don’t panic; instead, check same-day loans from a direct lender for guaranteed approval for emergencies. You may get instant cash to cover any requirements. You can do that without a guarantor or a collateral requirement. It thus helps you meet your needs without affecting the larger goal.

Step 5- Choose the right savings fund

Your saving preference may vary according to the timeline and the cash needs. You can set up an ISA for long-term financial goals like retirement. It may also push your personal savings allowance. Alternatively, you can also check FSCS protection, where you can save up to 85k without withdrawal penalties.

You can also use your current savings account or open up a new one for the focused fund allocation.

Step 6- Automate the savings

After choosing the right sinking fund type, set direct debits for the specific amount. It automatically gets transferred to the savings account after the salary gets credited. It helps you save towards the goal without worries.

Step 7- Track and Adjust the amount

You must analyse your finances and timeline to achieve the goal. Has the price of the article you wish to buy increased? If yes, then you must optimise the whole plan also. It may mean re-analysing your finances, budget, and resetting the amount goal. Yes, it may mean starting from scratch. It would not hurt your progress much.

Bottom line

This is how a sinking fund works. You just need to stick to a particular purpose to benefit from this. Set a specific amount to save after understanding the total costs. Likewise, adjust your budget, choose the right timeframe, and track your progress. Make changes (if you must) to achieve your goal in a timely manner.

Having worked as a research analyst for 10 years, Archie developed his interest in consulting people struggling to manage money and now working as a Financial Consultant at Onestoploansolution. He is postgraduate in banking and accounting. For his a normal day starts from assessing the application and helping borrowers with getting more control over their finances. Archie Leo contributes to the finance blog of the company where he has written a lot of articles covering a wide range of topics such as budgeting, investing, saving and building wealth. His goal is to make people’s life easier with money.